Private Credit: Reading Beyond the Headlines

Aureus Investment Perspectives | April 2026

Whether you are an avid follower of financial media or a casual consumer of mainstream news, it is likely that over the past couple of months, you have seen mention of trouble brewing in private credit. We take these concerns seriously and are using this quarter’s Investment Perspectives to dive into some of the most frequently cited issues and compare the hype to reality. Private credit is lending that occurs outside the traditional public debt markets and outside the traditional banking system. In practice, it means a non-bank lender, typically an alternative asset manager, directly provides a loan to a borrower through a privately negotiated transaction. We will first offer some opening comments on the off chance that everyone might not make it all the way to the end of our piece.

Credit cycles happen, but seniority is key: We want to acknowledge that we do not possess a crystal ball to help us divine the future. Credit cycles are a natural part of the economic cycle, and when they occur, lenders see elevated loan losses. However, for loans to a business, first-lien, senior-secured loans, the type found in Aureus directed private credit investments, are the last to absorb losses. Equity and subordinated debt bear the cost before “top of the stack” debt loses value. This makes private credit, as an asset, less risky than stocks.

Illiquidity is a bug and a feature: One particular focus of recent headlines has been on managers raising “gates” to limit investor redemptions, a measure taken to reduce strains on the invested portfolio and protect remaining investors. While a feature of semi-liquid “perpetual” Business Development Company (“BDC”) wrappers is the ability to redeem quarterly, they are structurally illiquid and should be treated as a long-term investment in an asset allocation. Some investors are only just awakening to this reality. Access to an attractive asset class without requiring the usual 10+ year commitment and the inconvenience of a capital call structure, is a significant improvement but does not come in fully liquid form. In return for accepting less liquidity, investors typically earn a higher yield.

Fear mongering generates page views: It is worth reflecting on why the private credit narrative sounds the way it does. The economics of financial media have changed profoundly over the past 15 years; subscription-supported publications that once competed on analytical depth now compete, alongside everyone else, for clicks, views, and share velocity on platforms whose algorithms reward engagement rather than accuracy. Fear, as a century of behavioral research confirms, generates more engagement per word than reassurance. A “cockroach” headline travels; a quarterly update on senior-secured loan-to-values does not. The practical consequence is that the volume of alarm reaching a client’s inbox or feed has become a deeply unreliable guide to the magnitude of the underlying risk. We believe this is a meaningful part of what is happening in private credit today; the fundamentals have softened modestly at the margins, and the narrative around them has hardened disproportionately. Calibrating to the former, not the latter, is one of the things we think a disciplined adviser is paid to do.

Concern #1: Private Credit Has Ballooned Into a Bubble

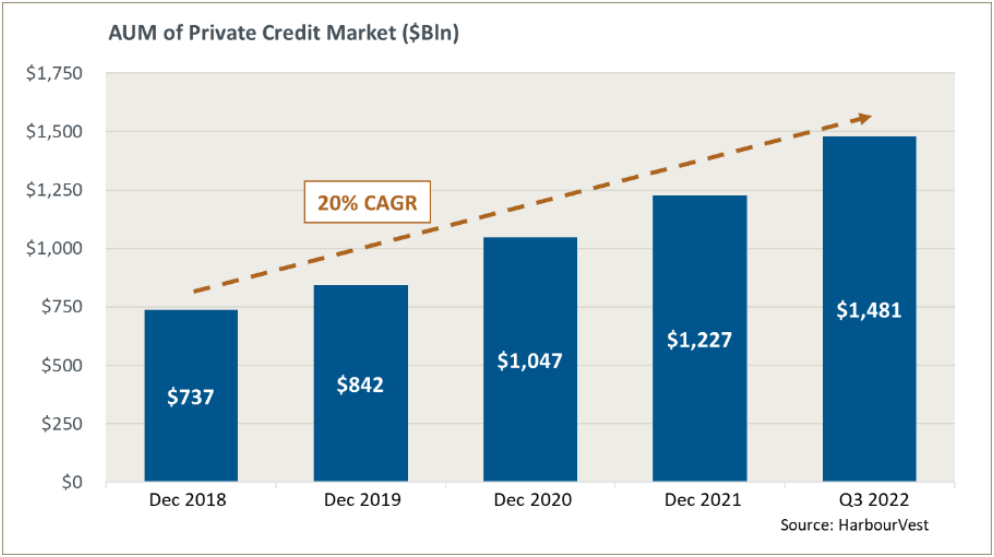

The Market’s Worry. Direct-lending vehicles have roughly tripled in size over the past decade; the broader private credit universe has crossed $1.7 trillion. Critics argue that a decade of zero interest rates pushed pensions, endowments, and individual investors into anything yielding more than cash, and that managers responded by raising ever-larger funds. The fear is a classic supply-driven bubble that ends in losses the models never contemplated.

Our View. Headline growth is real, but it is the wrong lens. Private credit represents roughly 4% of U.S. GDP. This is meaningful, but hardly systemic against the $15 trillion corporate bond market or the commercial banking system. Total non-financial corporate credit as a share of GDP sits at its 25-year average. What has changed is the composition, not the relative amount. Loans that banks used to hold on their balance sheets and syndicated paper that commercial lenders used to arrange have migrated to dedicated funds whose capital is locked up and matched to the underlying assets. On top of the size point, the capital stack itself has de-risked. Industry participants estimate that a decade ago, leveraged buyouts were typically financed with roughly 60% debt and 40% equity; today, the same deals are closer to 40% debt and 60% equity, meaning materially more equity cushion beneath the senior lender. Growth, in this case, is more a symptom of post-2008 structural reform working as intended rather than evidence of excess.

Concern #2: BDC Discounts and Redemptions Are Flashing Red

The Market’s Worry. Publicly traded BDCs—the only daily window into the value of the asset class—trade at a weighted-average discount of ~20% to stated Net Asset Value (“NAV”), a level reached only a handful of times in two decades. Some non-traded perpetual BDCs have reported redemption requests well above their quarterly limits (requests for 8-11% vs. a 5% limit), with many enforcing redemption gates to limit quarterly outflows. The inference is that reported NAVs will have to be written down materially, and the eventual realized losses will dwarf anything disclosed to date.

Our View. The discount is real; the inference is not. Public BDCs are small, retail-dominated, tax-burdened securities whose prices routinely overshoot the volatility of their underlying loan books by a factor of three to four. This is at least the eighth time in the past 20 years that the sector has traded at a 20%+ discount. In only one of those episodes, the cheap price correctly foreshadowed materially worse credit outcomes; in the other seven, the discounts reverted. Equally telling, fundamentals and stress gauges remain remarkably benign in the broader credit market, including the “junk bond” market. Currently, there are few signals of imminent, broader credit deterioration, and public leveraged-loan spreads have not widened as one would expect if credit were deteriorating.

On the redemption queues: We view this as headline-sensitive retail capital rotating out of semi-liquid wrappers following a frenzy of media headlines, rather than a credit signal. The 5% quarterly redemption limit in a perpetual non-traded BDC is, as Apollo recently reminded its shareholders, “an intentional feature.” The limit duration matches a roughly five-year investor horizon to the five-year weighted-average life of the underlying loan book. When demand spikes, the limit does what it is designed to do, honors the 5% gate and pro-rates the rest. Meanwhile, the underlying books continue to perform, with company fundamentals growing, interest coverage ratios improving, and non-accruals remaining historically low. When capital is locked up, paying its coupons, and matched to its liabilities, a fluctuating price in a thinly traded wrapper tells us less about credit than about who is selling and why.

Concern #3: The Software Reset Will Burn the Book

The Market’s Worry. Software is now the single largest industry exposure across public BDCs, at more than 20% of portfolio fair value. Much of the software composition is loans to sponsor-backed companies taken private at 9x revenue or more in the 2021–2022 vintage. Public software multiples have since compressed toward 3x, AI has introduced a credible challenge to the “durable recurring revenue” thesis, and dozens of 2021-vintage software LBOs with 2027 and 2028 maturities are trading at 75 to 80 cents on the dollar. If enterprise values continue to compress, a large share of the private credit universe is lending at a loan-to-value materially worse than the marks suggest.

Our View. This is the most legitimate of the four concerns, and the one where manager selection will matter most. Investors should not paint all software businesses or loans to software businesses with the same brush. This is because not all software businesses are equally at risk from AI, and not all loans were underwritten in an equally prudent manner. While the ultimate level of disruption to the software industry from AI remains unknown, several layers of protection are in place for investors. These include portfolio diversification, the need for equity and subordinated debt to be worth nothing before first-lien debt is impaired (based on industry data 60% of the enterprise value needs to be wiped out before the “equity cushion” stops protecting lenders), the potential for Private Equity (“PE”) sponsors to inject more capital to protect their reputation with portfolio companies, monthly financial updates from portfolio companies that allow for early intervention, and the potential for asset recovery in the event of a liquidation. These are the reasons loss rates for large lenders have averaged ~1% per year across cycles.

All that said, we think it is perfectly reasonable to expect some lenders to experience elevated default levels. Roughly 80% of middle-market private credit managers are designed to serve the PE sponsor community exclusively. In the 2021–2022 vintage, heightened competition led to tighter pricing, higher leverage, and weaker documentation. It is likely that when these loans come due in 2027–2028, some will require restructuring. Again, this is a manager selection problem, not an asset-class problem. Meanwhile, it is possible that stressed BDC portfolios that come to market will create secondary-market entry points at discounts that reflect forced selling rather than fundamental impairment, creating an opportunity for savvy credit managers.

Concern #4: Opacity, Leverage, and Interconnectedness = 2008 Redux

The Market’s Worry. First Brands and Tricolor—both recent bankruptcies—were the proverbial “cockroaches,” the first visible evidence of a broader infestation. Payment-in-kind (“PIK” – where in lieu of collecting cash interest payments, the principal amount outstanding grows) income has roughly doubled from pre-COVID levels and now represents approximately 8% of BDC income on average. Life insurers, newly tethered to alternative managers, sit atop pools of private loans whose true marks are unknowable. The cocktail of opacity, leverage, and interconnection is the one that turned subprime mortgages into a systemic crisis.

Our View. The comparison to 2008 sounds compelling but does not hold up to the numbers. Subprime vehicles before the financial crisis were levered at 90%+ against assets that proved to be worth a fraction of their underwritten values; BDCs today carry fund-level leverage of roughly 40–50%, with most operating at under 1x debt-to-equity. Private credit funds are financed with locked-up equity capital, not overnight repo, which means a spike in losses does not force a fire sale. Every BDC reports its full loan book—borrower, maturity, coupon, fair value—every ninety days, a level of disclosure the syndicated loan and high-yield markets cannot match. Realized loss rates at the largest direct-lending platforms have averaged roughly 1% per year over two decades, including through the Great Financial Crisis and COVID; Blackstone has cited a 21-year average loss rate of approximately 10 basis points on its own book. And the cockroaches, in fact, did not come from the private credit kitchen: First Brands and Tricolor were financed primarily in the bank-led syndicated loan and asset-backed markets, not by direct lenders.

PIK deserves the attention it is getting, but levels vary widely by manager. PIK ratios across the peer group ranged from ~1% at the low end to nearly 18% at the high end. This is where manager selection plays a key role. With the managers selected by Aureus, PIK accounts for only 1-3% of total income, well below the industry-wide 8% aggregate. Further on manager dispersion, the Fitch-rated BDC universe shows a 1.1% average loan loss rate, but that falls to 0.5% when you exclude the two weakest managers.

In Closing

None of this is an argument that private credit is without risk. Default rates will rise from today’s low base; individual managers will disappoint; certain retail-oriented wrappers have been built for a market environment that no longer exists, and those wrappers—not the strategy—will continue to produce uncomfortable headlines. The point-by-point exercise above is not intended to dismiss any of that. It is intended to distinguish between risks that are reasonably priced and those that have been amplified by a narrative in search of a crisis.

On balance, we believe the headlines overstate both the novelty and the severity of what is actually happening. The asset class is larger, better disclosed, and more appropriately financed than at any prior point in its history. The most visible signal of stress—BDC discounts—has a long record of marking entry points rather than exits. And the best underwritten senior-secured loans, held by managers we know and have diligenced, still offer yields in the high single digits with loss-adjusted returns we believe are difficult to replicate elsewhere in today’s fixed-income landscape.

Our manager selection process continues to lean on three criteria: (1) a multi-cycle track record and a demonstrated willingness to use covenants to protect principal; (2) originated, senior-secured, first-lien exposure with conservative documentation; and (3) a capital base appropriately matched to the underlying assets rather than reliant on daily retail demand. We continue to regularly engage directly with the managers our clients hold during this period.

Aureus partners, employees, and families are investors with these same private credit managers, and we remain watchful, but comfortable with the positioning. As always, please reach out with any questions or if you would like to set up a time to discuss this topic in more depth.

This commentary reflects the opinions of Aureus Asset Management as of the date of publication and is subject to change without notice. It does not constitute investment, legal, or tax advice, nor a recommendation to buy or sell any security. Statistics are drawn from sources believed reliable, including The Economist, Callodine, TCW, Blackstone, Apollo, Cliffwater, Fitch, and public BDC filings, but accuracy is not guaranteed. Past performance is not indicative of future results; private credit investments are illiquid and involve substantial risk of loss.